2020<span>Twenty Twenty</span>

Expansion Saas Benchmarks

Data for objective decision making at the expansion stage

Get the FULL ReportData for objective decision making at the expansion stage

Get the FULL ReportThe road to market dominance doesn’t look like every chart in an investment deck—up and to the right. The road also doesn’t look like every software S-1 (cough, Snowflake), or like a pre-money valuation of more than $200M at just $1M annual recurring revenue, or 50x+ next-twelve month revenue multiples (we’re looking at you, Datadog) or accelerating growth rates at scale (that’s you, Zoom). Often founders are confronted with challenges that never see the light of day, leaving their operator peers without the objective benchmarks required to make strategic decisions that accelerate long-term growth.

To help folks make better operational decisions, we’re releasing the results of our fourth annual Expansion SaaS Benchmarks survey. This report was designed specifically to enable operators to compare themselves against their exact peers across the metrics that matter most in a SaaS business.

This year’s report includes data from more than 1,200 respondents from around the globe, including more than 400 respondents this year alone. It revealed surprising insights about what’s on everyone’s mind: How did software companies adapt, and what has been the impact of the COVID-19 crisis? We also revisited topics such as founder attitudes, the adoption of product led growth (PLG), progress on executive diversity, how founders really feel about their VCs, and much more. We’re excited to share this report, as well as all of our detailed insights for download.

Participants in the 2020 Expansion SaaS Benchmarks ranged from <$1M to $150M+ ARR publicly traded SaaS companies. The majority of respondents were the CEO / Founder (39%) or Head of Finance (29%). Nearly two-thirds of respondents were from companies that predominantly sell to Midmarket or Enterprise customers (100+ employees).

For questions, comments or to participate in next year’s survey, please email Sean Fanning at [email protected]

All the way back in 2018, we asked, “Is Enterprise SaaS recession proof?” In 2020 we finally got our answer: Yes. The United States economy is officially in recession, Q2 GDP shrank -32.9% on an annualized basis, and of course unemployment has peaked at historic levels. Plus, renewed tensions between the US and China as well as the presidential election have weighed heavily on investor sentiment throughout the year. But Enterprise SaaS is still partying like it’s 1999.

These levels would have made a sane investor faint just a few months ago—and, sure, interest rate policy plays a role. Between the NASDAQ and SaaS index setting all-time high after all-time high and SPACs, direct listings or IPOs galore, we have to ask: What is driving the public market exuberance for software businesses? In the midst of recession 11 enterprise SaaS companies filed or actually priced their initial public offerings, on par with 12 in 2019 and approaching the high water mark of 16 in 2018.

The companies that are going public in 2020 are extremely impressive. They’re largely growing faster, growing more efficiently, raising less capital at scale, and getting to be on average older compared to previous cohorts. (All of this is especially true when you account for outliers like Zoom in 2019 and Snowflake in 2020.)

SaaS companies are getting better and at the same time folks better understand B2B markets, unit economics and payback periods are more clearly defined, and overall future price uncertainty of the assets seems to be reduced. This has created exuberance in the market.

Plus, as we’ve come to find, the digital transformation mega-trend is a real thing. Microsoft’s CEO claims to have experienced “two years of digital transformation in two months” and Nike realized its ecommerce sales goal three years ahead of schedule. The world doesn’t just run on Dunkin (can you tell we’re from Boston?). It also runs on software.

How do operators translate the public markets to their $5M SaaS business, and how has COVID played out in the private markets? TL;DR: the bark was worse than the bite.

While COVID took its toll, it wasn’t as bad as many predicted. 34% of our survey respondents noted a “moderate negative impact” (-10 to -24% impact vs. original budget). But “just” 27% noted an impact greater than -25% (vs. their original 2020 budget). The remaining 39% either noted a small negative impact (18% of respondents, a 0-9% negative impact vs. budget) or even a positive impact (21%). SaaS companies in the collaboration and ecommerce sectors fared particularly well during this period.

We’re encouraged by how proactive companies were in changing strategies, which likely helped to stave off the worst impact in March and April. The most popular responses to our question “Which defensive tactics have you adopted in response to the COVID crisis?” were (1) cutting discretionary spend (60%), (2) relaxing payment terms (47%), and (3) renegotiating vendor contracts (44%). On the flip side, many companies went on offense by shifting marketing strategies to address new use cases (61%), adopting more flexible contract terms for new customers (57%), or changing product roadmaps to target new use cases (46%).

As expected, growth rates for companies across all ARR stages, from <$1M to $100M+, decelerated somewhat. The median company reported 42.5% year over year growth as of June 2020, vs. 48% and 53.5% in 2019 and 2018, respectively. It’s been easy to write off 2020, but getting back to work ahead of 2021 is key: how you’ll get back on a hyper-growth trajectory and what your business will look like in the future is critical.

In our view, it’s time to ramp back up GTM investment. Companies are acquiring and retaining their customers as efficiently as ever. They’re just not spending nearly enough on acquisition to actually reach those customers who have demonstrated they still want to invest in digital transformation.

While 1H 2020 sales and marketing budgets decreased by 14% and 25% vs. 2019 and 2018, respectively, CAC payback has remained remarkably consistent. And net retention even improved slightly as companies shifted focus from acquisition to retention. With the potential exception of companies serving industries that were forced to shut down (for example retail, hospitality or restaurants, like Toast) once customers reach their “aha” moment with software, products become mission critical and it’s nearly impossible to go back to the old way of doing things.

| Growth Rate | Sales Spend as % of Rev | NDR | Payback (Months) | |

|---|---|---|---|---|

| 2018 | 54% | 40% | 100% | 12 |

| 2019 | 48% | 35% | 99% | 11 |

| 2020 | 43% | 30% | 102% | 11 |

It is clear that companies responded to COVID with an abundance of caution. With hindsight bias, many companies may have actually overreacted. Now, some are faced with a scenario where competitors are leapfrogging them because they pulled back on growth initiatives while competitors kept going. At this point, the data prove that demand remains strong. Start investing again to get back on your pre-COVID growth trajectory and make your 2021 an accelerating growth year.

As you consider ramping go-to-market back up, why not finally lean into product led growth (PLG)?

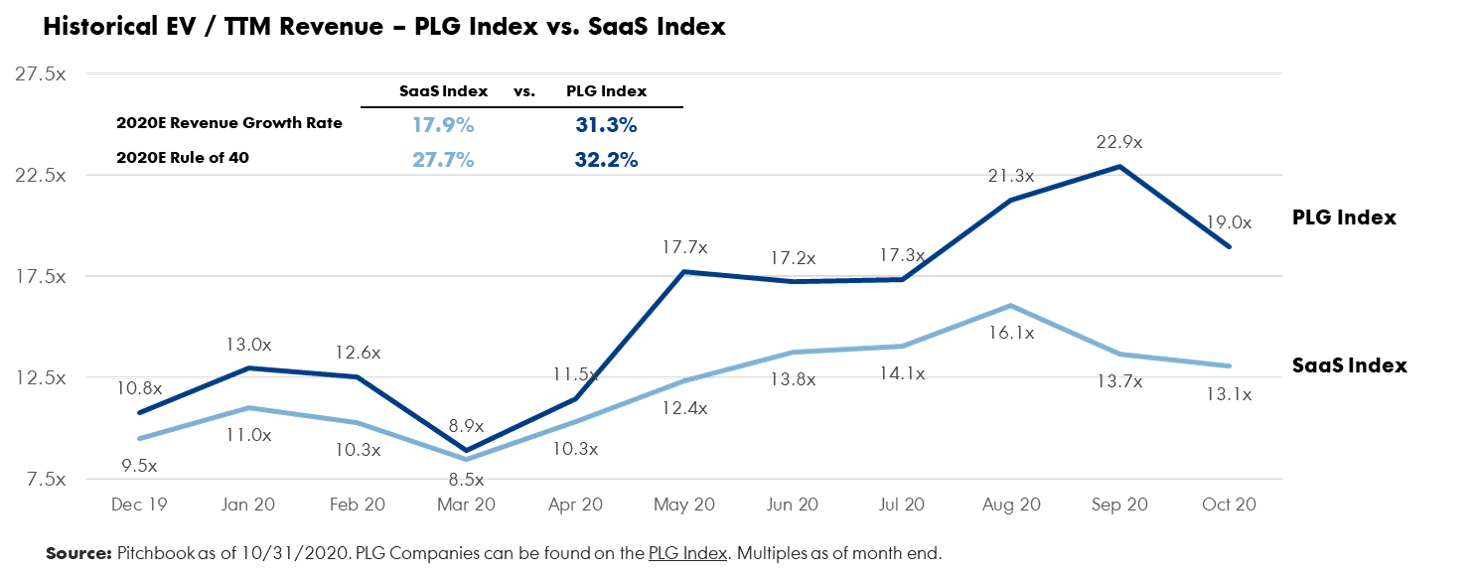

In 2020, remote work has forced employees to be self-sufficient and has driven individuals to seek out products that solve their everyday challenges. This is the type of end-user focus that the product-led model rallies around. Product-led companies are always “open for business,” and their lower entry prices are less susceptible to budget cuts. In fact, the SaaS companies in our PLG Index trade at a nearly 50% premium to the broader SaaS index, proving that product-led revenue is more valuable. As your company ramps back up GTM, PLG can differentiate you.

Despite the obvious success realized by “pure play” PLG companies, most companies have only dipped their toe into leveraging various PLG tactics. Four-in-five survey respondents said they’ve adopted at least one PLG tactic (for example, a free trial or product analytics for decision making), but only 27% of companies admit that product led growth is fundamental to their business. This is down nearly 20% from last year.

We’ll say it again for the people in the back: Free trials and product analytics are table stakes. Having a free trial doesn’t mean your business should immediately be rewarded with a premium valuation multiple. Recent S-1’s demonstrate how entire organizations—across product, engineering, sales, marketing and success—need to be bought in on this strategy. PLG is more than a go-to-market strategy—it’s a business strategy that puts the end user’s needs first.

As Jfrog wrote so eloquently in their recent S-1 filing, “Importantly, we’ve never sold it. It’s always been bought, and to this day we haven’t made a single field sales outbound call to a prospective customer.” Their filing has many more quotes that detail how they’ve built their business around the pillars of PLG:

Don’t conflate the idea of starting with one user on a free product as automatically resulting in lower ACVs, smaller target customers and bad retention. PLG companies report nearly identical target customer profiles as other SaaS businesses; 62% of PLG companies target midmarket and enterprise customers (>100 employees) vs. 69% of non-PLG companies.

PLG companies land with a lower CAC at more digestible ACVs to start, but are able to drive significant expansion in accounts over time as the product spreads throughout large organizations. While just 15% of PLG companies sub-$1M ARR have ACVs above $25k (vs 59% of non-PLG companies), this balance flips at scale. Once PLG companies are generating >$50M in ARR, 66% of them generate ACVs above $25k compared to 75% of their non-PLG competitors. This is reflected in the strong net dollar retention rate of PLG companies (105% vs. 98%). PLG companies can be much less specific in their ideal customer profile as they search for product market fit, and over time target high value customers specifically and more efficiently.

As you consider ramping go-to-market back up, why not finally lean into product led growth?

Whether you’re just starting out or you’re a mature company looking to pivot to PLG, it’s happened before! It’s far more challenging, but that doesn’t mean it can’t be done. Success stories like HubSpot, Zipwhip and OutSystems teach us to (1) start with a low-risk opportunity, (2) generate early wins, (3) use the learnings to improve the product for all customers.

Last year we advised that in an uncertain world, let’s make profitability cool again. Now surely we couldn’t have predicted a pandemic, but the data don’t lie: being able to control your own destiny with unit economic profitability and control of spending translated into companies being able to mitigate impact more proactively.

In any software business sales & marketing and product & engineering are the two largest buckets of expense. Companies responded to COVID by decreasing sales and marketing spend by 14% YoY. While go-to-market spend and headcount was immediately and aggressively cut, engineering heads were spared from COVID related RIFs.

Engineering headcount has remained a black box where money disappears for many companies. Public companies continue to spend 31% of revenue on product and engineering, and the median respondent to our 2020 survey spent 30% of revenue on product and engineering, which is identical to the data from both our 2018 and 2019 surveys! If we’re to believe the whopping one-half of founder respondents who claim they’re worried about product execution, then it’s time for teams to start holding product teams to the same standards as commercial ones.

With the rise of PLG, product and engineering has become far more influential in how SaaS companies acquire, convert and expand their users. Product may already own a self-service revenue number, but this doesn’t always get filtered down to how teams are managed. Companies like Divvy already push PMs to own revenue, but that isn’t the norm in SaaS. Here’s what we recommend if you’re just starting out:

Set business impact KPIs that the management team monitors weekly/monthly (product-influenced revenue, product influenced word of mouth / referral acquisition, revenue attribution to feature, team velocity, product quality indicators).

Sprint planning starts to get tied to these KPIs and each sprint has an expected return profile that exceeds the company’s hurdle rate.

Reward the best team members with financial upside when they drive impact in the product funnel. The best sales reps can make $300-400k+. When will we see the same thing with great PMs (albeit probably with equity compensation to drive the right incentives)?

We’re huge fans of the tried-and-true SaaS metrics: ARR growth, CAC payback, net dollar retention and many more. But they’re not enough in the product-led era, whether you consider yourself PLG or not.

Ask yourself: Do you really know where your engineering spend is going and how it’s creating value? Whether your team owns revenue targets yet and regardless of whether you even consider yourself a PLG business, your engineering team is a revenue-generating bucket of expense. If users discover your product via referral from an existing user, land on your website organically, sign up for a product without speaking to a sales rep… your product has served as a means of customer acquisition!

It’s time for new metrics: return on incremental invested capital and the Natural Rate of Growth.

Start by measuring return on incremental invested capital (ROIIC, similar to burn productivity). While we’re all familiar with the adage that revenue growth and Rule of 40 are correlated with valuation, these metrics ignore the 30%+ of product & engineering expense that is driving growth. Until you measure all of the cash going towards customer growth and retention, you’re not able to make the correct tradeoffs between investment opportunities (whether that is in sales, marketing, success, product, engineering… or even M&A instead!). ROIIC measures the ratio between gross profit added (less general and administrative expenses, which aren’t growth expenses) and sales & marketing plus product & engineering spend.

Similarly, a company’s Natural Rate of Growth (NRG) is critical. One way to think about it is how fast a company grows without even trying—before layering on incremental investments in sales and marketing. We’re looking to pinpoint the percentage of your recurring revenue that comes from organic channels and starts with your product. Mature product-led businesses outpace other SaaS companies in both growth and Rule of 40, but younger product-led businesses may not always stand out when you apply some of the CIO-era SaaS metrics we’re used to using. That’s why we set out to create a metric that would identify a business’s Natural Rate of Growth (NRG), how efficiently the growth engine inside of a business (aka its product) is running when you peel away sales and marketing efforts.

When we examined organic acquisition, one of the components of the NRG metric vs. sales-led acquisition, the results were stunning: Slower growing organizations lean on sales-led acquisition strategies more than companies with high growth rates. In turn, companies that have taken a product-led, go-to-market approach tend to have higher proportions of organic traffic.

| ARR | Good | Better | Best |

|---|---|---|---|

| $1-10M | 50-100% | 100-150% | 150%+ |

| $10-50M | 30-50% | 50-100% | 100%+ |

| 50M+ | 15-30% | 30-50% | 50%+ |

With capital more abundant than ever, more founders are raising than ever. 84% of respondents this year noted they’ve raised venture capital, and 25% more vs. 2019 had raised within the last six months alone. But there are more alternative funding options than ever, too. We’re not just talking about direct listings and SPACs. With the advent of the rolling fund, the “super angel,” recurring revenue syndication, funding for bootstrapped “micro SaaS” companies, and venture debt becoming a crowded market, founders have many ways to finance their business. Equity is actually the most expensive.

So we had to ask: With so many alternatives, do founders even like their venture investors? Reviews on sites like VC Guide suggest maybe not. Visible data found that the average VC NPS score of 23 falls below the average for the airline industry. As they noted, “This is not a great industry to be compared to in terms of customer satisfaction scores.” Our data confirm our hypothesis: 30% of founders would not recommend their venture capital firms, and another 31% were neutral on their VC partners.

Only 15% of founders noted they’re concerned about fundraising (down 32% from last year), so in this seller’s market with venture capital more abundant, a dollar is still just a dollar. Founders must look beyond the round size and valuation. What value do venture investors really add to your business? Will they and their extended team roll up their sleeves and help you invest each dollar of their capital more effectively and turn $1 from them in $2, $3 or $4 dollars of equity value? Much has been written in the wake of Snowflake’s IPO about the incubation model at Sutter Hill Ventures, and Kevin Wok wrote about just how important “the value over replacement player” in fact is in venture capital, adding that “firms do this most notably by providing capital, but also by other methods like lending their brand or directly helping with operations.”

Quantifying VC “value-add” is challenging, so we created a simple 5-step framework to help you choose a term sheet. The question is multivariate: “Who has the best terms” (quantitative) and “Who is my preferred partner” (qualitative). And the two don’t always map—the preferred investor might not have the most compelling offer. By reframing the question as “How much more valuable of a company can I build by working with my preferred partner and the capital they provide,” you’ll get to the right answer.

When it comes to remote work, just 1% of companies in our data were remote before COVID. And while all companies are unavoidably “remote first” now, founders aren’t liking it. Reed Hastings (Netflix CEO) isn’t alone in deeming remote work “a pure negative.” 58% of founders would not recommend remote work given what they now know. Perhaps this “never going back to the office thing” is all hype after all? We come out somewhere in the middle of the “cities are done” vs. “cities are the future” argument: OpenView research proves 72% percent of employees value flexible work policies—the ability to work from home or have a day to get the car fixed without logging PTO is what employees really care about.

As office reopenings (hopefully!) accelerate later this year and in the early half of next, articles like this resource from HBR are starting to emerge on leading teams in a post-pandemic world. When we do “go back to work,” OpenView’s Talent Team recommends four key things to ensure a successful transition:

Historically, we’ve reported on gender parity at the Leadership and Board level, but last year we began collecting data on underrepresented minority founders. We’re disappointed to see that after stagnation last year, progress towards more diverse leadership teams and boards remains underwhelming.

The one bright spot: 42% of respondents had one or more female BoD members, which is up from 38% last year and nearly 50% more than in 2017. We suspect that part of the driving force behind this shift is government intervention, including California’s boardroom diversity law that was signed in 2018. Otherwise only 14% of companies had gender parity in leadership (unchanged from 2019) and 6% had gender parity on the BoD (down from last year). To put the gender gap in perspective, research shows that there are fewer women among Fortune 500 CEOs than there are men named James.

While progress on gender diversity has been slow—albeit steady—we’re encouraged by the cultural momentum around ending systemic racism and committing to racial and ethnic diversity, equity and inclusion. It remains to be seen whether this activism will translate into meaningful representation within positions of leadership in SaaS. In this year’s survey, 45% of companies had 1+ Black, Hispanic/Latinx or Native American member of their leadership team (abbreviated as underrepresented minority or URM in the chart below) and even fewer (27%) had 1+ underrepresented minority BoD member. We are far from equal representation, and we’ll continue to report racial and ethnicity data in our survey going forward.

We’ve said it here before and research continues to show that diverse teams perform better (faster growth—and these days in SaaS, does anything else matter?) yet still raise less capital than their homogeneous peers.

| 2017 | 2018 | 2019 | 2020 | |

|---|---|---|---|---|

| 1+ Female BoD Member | 29% | 37% | 38% | 42% |

| Gender Parity in Leadership | 12% | 13% | 13% | 14% |

| Gender Parity on BoD | 4% | 8% | 8% | 6% |

| 2020 | |

|---|---|

| 1+ URM BoD Member | 27% |

| URM Parity in Leadership | 8% |

| URM Parity on BoD | 7% |

Capital is cheap today. Mortgage rates are low, governments are selling cheap debt, and venture dollars chasing startups are more abundant than ever. The cost of capital is as low as it has ever been and it will perhaps never be cheaper to finance a SaaS company. So we pose this question to founders: where would you invest differently than you are now with this knowledge? What investments might you double down on (cough… PLG)? How can you start positioning your post-COVID narrative today for a capital raise in 3, 6, or 12 months? How can you monitor your business in new ways that more appropriately reflect the value your investments in sales and product are creating?

We’re in an entirely new world. Everyone must start getting used to this new normal for SaaS multiples and lean into what the “why” behind it: digital transformation tailwinds, more capital chasing opportunities, and better understanding of how SaaS companies grow. Let our fourth annual SaaS benchmarks survey be a roadmap for where to start.

© Copyright 2010-2020 OpenView Venture Partners.<br /> OpenView® and OpenView Labs® are registered trademarks that are used under license by OpenView Venture Partners. All Rights Reserved.