Private Equity is Your New (and often best) Exit Opportunity

November 7, 2017

Last year Salesforce went on a SaaS buying spree. The CRM giant gobbled up the likes of Demandware ($2.8B), Krux ($800M), Quip ($750M), Beyondcore ($110M) and at least eight other technology companies. This year, they haven’t made a single notable SaaS acquisition to date.

And Salesforce isn’t the only major strategic sitting on the sidelines. Oracle made nine acquisitions in 2016, including Netsuite ($9.3B), Textura ($600M) and Dyn ($600M). This year they’re down to only three according to data from Crunchbase. Likewise, IBM went from thirteen acquisitions last year to a measly four in 2017 (at the time of this article’s publication).

And Salesforce isn’t the only major strategic sitting on the sidelines. Oracle made nine acquisitions in 2016, including Netsuite ($9.3B), Textura ($600M) and Dyn ($600M). This year they’re down to only three according to data from Crunchbase. Likewise, IBM went from thirteen acquisitions last year to a measly four in 2017 (at the time of this article’s publication).

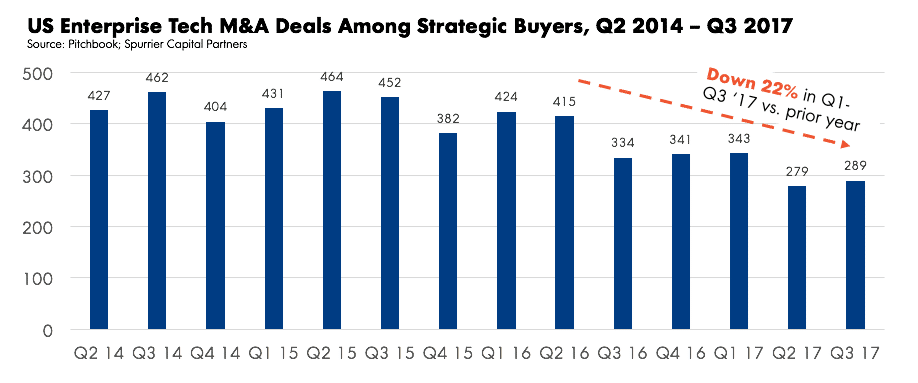

This downturn is more than just an anomaly. While venture funding continues to flow to startups, strategic buyers have done 20% fewer deals, from 1,173 to 911, over the last year.

Strategic buyers have hit the pause button for a few reasons. Some, like Oracle and Microsoft, still have to digest their previous acquisitions. Others still might be concerned with high prices and are hoping to wait the market out (possibly predicting an evitable cooling). The rest might be waiting out fiscal and regulatory uncertainty. Regardless of their underlying reasons, the slowed deal pace adds up to troubling news for enterprise technology founders looking to find suitable homes (or exit outcomes) for their businesses.

With strategic buyers sitting on the sidelines, you might look to public markets for liquidity. Unfortunately, despite signals that 2017 would be a banner year, enterprise tech IPOs remain few and far between. There have been some notable successes – Okta, Mulesoft, MongoDB come to mind – but the bar to IPO remains exceedingly high. The median 2017 IPO had $133M in prior year revenue and 55% year-over-year growth. Most venture funded SaaS companies don’t meet such lofty expectations.

Private equity isn’t your enemy; it’s your new exit opportunity

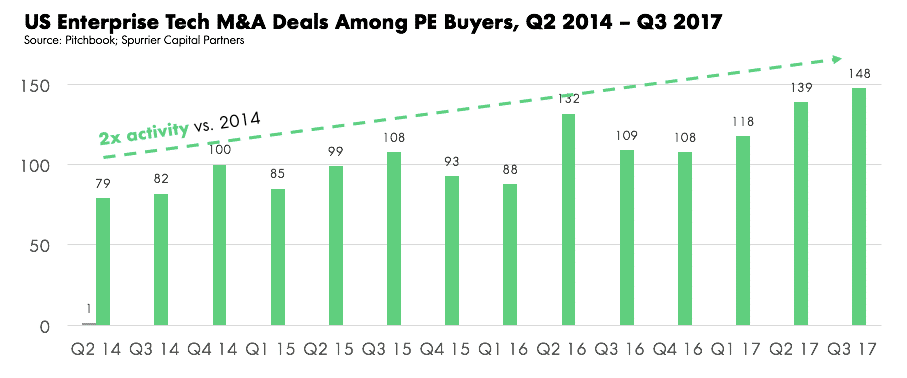

The good news: private equity has stepped into the chasm, doubling enterprise tech deal activity since 2014 – the result of several favorable market trends.

1. Technology-focused private equity firms have raised record-setting sums of money.

The top 20 PE firms now sit on an estimated $349B in dry powder, up from $260B in 2016. Meanwhile, firms like Francisco, Thoma Bravo, Vista and others are increasingly adding lower and midmarket mandates into their investment strategy. Even more favorably, we’re seeing generalist PE firms growing more interested in enterprise tech.

2. There’s an outdated view of private equity firms focusing largely on turnarounds, paying low multiples and ruthlessly cutting costs out of a business.

Today’s enterprise tech PE buyers are different. Given the low cost of capital and competitiveness of deals, they’re willing to pay up for good companies. Take SolarWinds and Cvent for example. Bloomberg reports that they were acquired for 9.1x and 7.1x multiples, respectively.

3. PE firms aren’t just looking purely at EBITDA anymore, either.

The tried and true high EBITDA, low growth and highly levered (i.e. LBO) deal is still part of the PE repertoire; however, they are increasingly open to strategic deals and high growth companies. Take Thoma Bravo’s acquisition of Qlik Technologies last year. They paid $3B, or 200x core earnings, because the company was still growing licensing revenue 20%+ year-over-year (on a constant-currency basis). For these deals, private equity firms want to see an attractive balance between growth and profitability with a favorable ‘Rule of 40’. In other words, it might be okay to be break-even or even still burning cash so long as you’re growing nicely and have a clear path to future profitability.

Let’s not forget, the deal dynamics of selling to PE are also quite attractive. There’s far greater certainty and speed of close compared to corporate M&A. It’s cleaner than an IPO, requiring less preparation, less regulatory burden, no public position to unwind and no dilution. Plus, PE firms’ equity role offers another bite of the apple to accelerate growth.

How to position your company for a successful PE outcome

There are steps that every software company can take to position themselves for a successful outcome, without putting up a for-sale sign. (In fact, we put together a playbook on the topic that you should check out.)

First and foremost, take the necessary steps to ensure that your financials are attractive to PE buyers. That means pursuing balanced, efficient growth and the Rule of 40 rather than a ‘growth at all costs’ mentality. Meanwhile, make smart investments in customer success and retention. Sticky, predictable recurring revenue is of fundamental importance to many PE buyers.

Tailor your story appropriately for what a PE buyer will care about. Your standard corporate deck might fall on deaf ears if you’re not thoughtful. Consider how a PE firm might be able to make a healthy return on their investment post-acquisition. For example, could you be positioned as an attractive platform play, rolling up several smaller companies in your space? Is there an inflection point story for your company, i.e. an opportunity for PE to apply their operations teams, acumen and/or capital to generate value that the existing investors can’t?

As you put the fundamentals in place and craft your story, start meeting with PE firms. Introductory meetings should take place well before you plan to sell. You’ll get to know different PE buyers and give them a chance to get to know your business. You might find that no two PE firms look the same and it’s important to find a firm that fits your culture, shares your objectives and has the right expertise.

And if you’re lucky (and smart), you might just find your ideal exit opportunity.

Looking to up your chances of being acquired by a PE firm? Check out our eBook below.

![]()

In this playbook you’ll learn:

- The key steps you should be taking right now, and in what order

- How to build a corporate deck that generates buzz around your company

- How to identify and prioritize the target acquirers for your business

- Ways to break in, including email templates that have worked for others

- The right time to engage an investment bank and what to look for