New Relic’s IPO Filing: An Analysis of SaaS Growth Drivers

November 12, 2014

Let’s take a look under the hood: What the New Relic’s S-1 reveals about the SaaS company’s key drivers of growth

Together with David Skok and Pacific Crest, our team recently completed a comprehensive financial benchmarking survey of the SaaS industry. Besides providing a rich dataset that’s spurred a lot of discussion around SaaS metrics, one of the main goals of the survey was to provide operational benchmarks for management teams for their financial planning as well as financing strategy.

So when we got news of Monday’s two high-profile IPO filings — New Relic and Hortonworks — we thought, what a great opportunity to battle-test our own benchmarks as calculated from the survey. Both companies are hot startups considered to be among the leaders in their respective markets, both in terms of product leadership and market shares. By taking advantage of the financial and operational information disclosed in their S-1 filings, we can see how they line up with the rest of the industry.

Note: We do need to point out that it’s impossible to expect the comparisons to be dead-on. While New Relic is a classic business SaaS company, Hortonworks has a professional open-source model that relies heavily on support subscription and professional services.

With that caveat in mind, let’s dive into New Relic’s numbers first.

Breaking Down New Relic’s Numbers

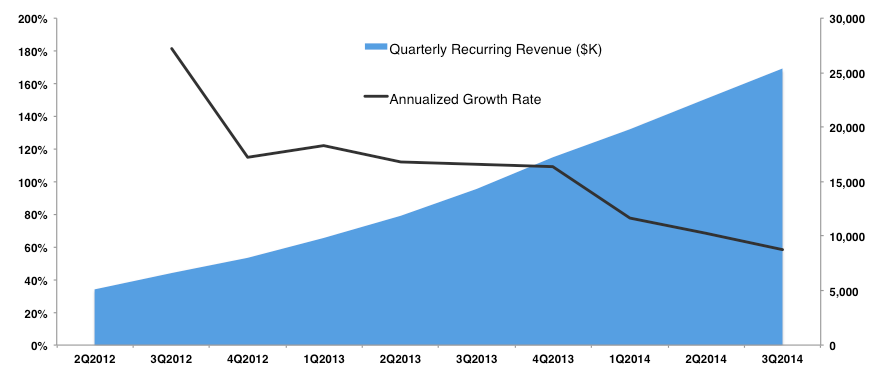

Quarterly Revenue & Annualized Revenue Growth

Given the very limited annual financial data typically reported in the S-1 filing, we opted instead to look at quarterly data, which presents a much more granular level of details. In terms of quarterly revenue growth rate, New Relic has enviable growth, as shown in the chart below:

New Relic Quarterly Revenue and Annualized Revenue Growth

The company’s annualized growth rates in 2012 and much of 2013 were an incredible 100%+, despite the fact that it was already growing past $40M in annual revenue at that point.

When compared with the broader dataset from our survey, it is clear that New Relic is an outlier — probably ranking in the top 5-10% of SaaS companies with similar revenue scale:

Source: Pacific Crest 2014 SaaS Survey and David Skok’s ForEntrepreneurs.com Blog

The charts above are a powerful justification of some of the extremely high valuations we are seeing in the current market. Companies like New Relic can grow from a few millions dollars in revenues to tens of millions of dollars in just a few years. On top of that, companies that achieve that growth far outpace the rest of the industry, and quickly become the dominant new player in their space, thereby securing the majority of the value to be created in its markets.

Venture investors therefore are encouraged to look for those superstars and bet heavily and early on them.

Digging Deeper

So how did New Relic achieve such dramatic growth rate? Let’s dig deeper by looking at four financial ratios:

- Gross Margins Percentage

- Research and Development Cost as a Percentage of Revenue

- Sales and Marketing Cost as a Percentage of Revenue

- Annual Net Dollar Retention Rate

To compare apples to apples, we have to calculate the median value for each of those metrics, looking at companies that are at the same revenue run rate as New Relic, and compare those benchmarks with each of New Relic’s corresponding ratios, for each of the quarters starting in Q2 2012. The benchmarks have to change from quarter to quarter, because in later quarters, the comparison set needs to comprise of larger companies to match New Relic’s increased revenue run rate.

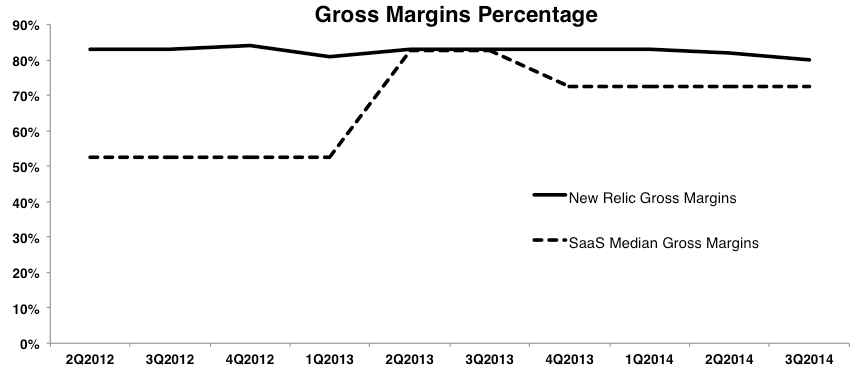

Gross Margins Percentage

Most SaaS companies, like other software businesses, tend to have high gross margins. However, in certain stages in their maturity, they have to accept gross margins compression, because of price pressure, increased costs of revenue due to services and support costs, or hosting costs that scale up faster than revenues. For New Relic, however, we can see that the company has had a remarkable run of very high, almost constant gross margins of about 83%.

Many things can possibly contribute to this remarkable result, such as continued product innovation to maintain product leadership (and therefore a price premium), optimization of hosting costs as they’ve scaled up, or continued control of support and services costs by maintaining the product’s ease of use and using self-help features.

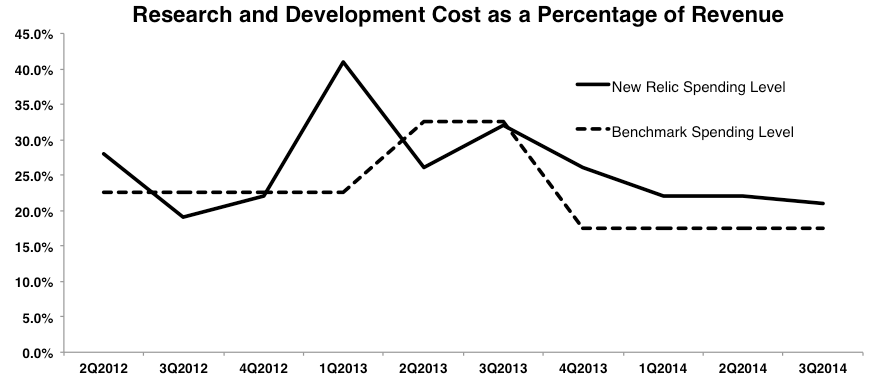

Research and Development Cost as a Percentage of Revenue

The common, accepted wisdom is that research and development scales quite linearly with the size of the company, with startups spending about 23% of their revenue on R&D in the early years, and about 18% of their revenue on R&D once they pass $100M in annual revenue.

In this respect, although we can see that New Relic does not follow that exact trajectory, their R&D spending levels do follow a similar evolution of starting at over 20% and gradually going under 20% as the company has scaled up.

We do need to note, however, that the company’s revenue was growing very quickly during this period, and that means their R&D spending actually grew very quickly as well, instead of lagging the revenue growth. It surely did not hurt the company, as they were able to invest more into their product to maintain their leadership, which might have led to all of the good effects on their gross margins as discussed above.

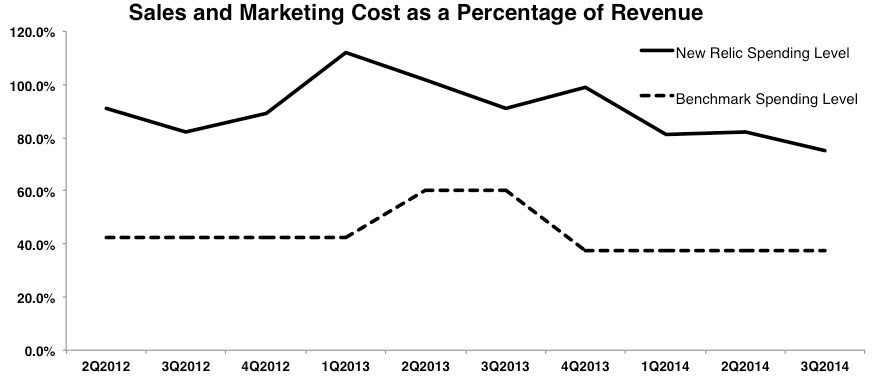

Sales and Marketing Cost as a Percentage of Revenue

The chart shows a clear, drastic difference. New Relic spends above twice as much — as a percentage of their revenues — on sales and marketing as the typical SaaS company of the same size among the 400 that we surveyed. Moreover, they also maxed out their spending a little earlier than the benchmark would have suggested.

While in more recent quarters, sales and marketing spending has come down gradually — and we should expect that trend to continue — it is still vastly higher than what most of companies at their level are doing. It is also actually quite high compared other SaaS companies that have recently gone public, such as Hubspot.

Clearly, there is a correlation between New Relic’s spending level and its growth, but one might wonder whether there is causality in the spending level and the growth, or whether it might just be that the company scaled up its spending based on the revenue that it was generating, and that the growth is really driven by a huge market’s appetite for a winning solution. Moreover, because business technology buying cycles may take months or even quarters, sales and marketing investments typically only result in actual revenue growth after one or two quarters, and we therefore need to look at the lagged correlation between sales and marketing spend and revenue growth.

That’s a topic for another blog post, when we can dive deeper into the sales and marketing economics of New Relic. But for now, there is one additional thing we believe has been a powerful driver of New Relic’s growth — its ability to grow and retain its existing customer base.

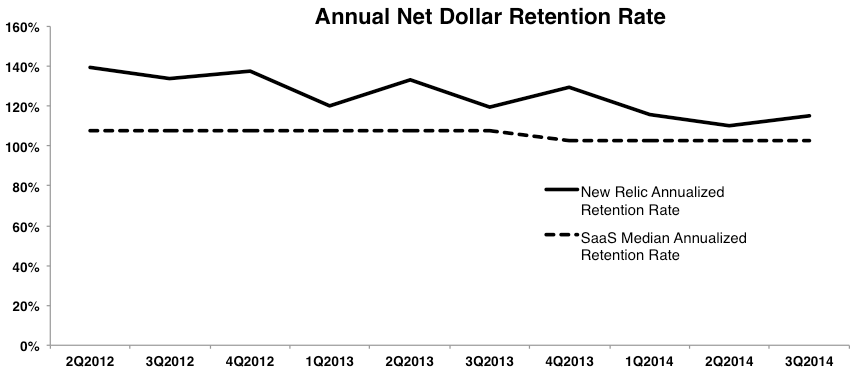

Annualized Net Dollar Retention Rate

This metric shows how much the billings for a specific cohort of customers grows after one year, after taking into account cancellation and downgrades, as well as upgrades and upsells. This is where New Relic appears to outperform its peers consistently, and even though the rates have come down somewhat, they are still above the median and contribute healthily to the company’s growth.

What Do You Think?

Do you think New Relic will have a successful IPO? Did we miss any interesting data points from their S-1? Please share your thoughts in the comment below.

Image courtesy of NASA on the Commons