How a Price Change Can Impact Your SaaS Metrics: Example in Action

July 14, 2015

In an earlier post, “Predicting the Impact of SaaS Pricing Changes,” we looked at how price changes can impact SaaS metrics and what questions you should ask before making a price change.

Let’s look at what happened at some real companies when they made price changes.

The critical metrics we are concerned with are Customer Acquisition Costs (CAC), Customer Lifetime Value (LTV) and Monthly Recurring Revenue (MRR) — the classic SaaS metrics (to refresh your memory see David Skok SaaS Metrics 2.0). Are these the only metrics you need to be concerned about as you manage your business? Of course not. You also worry about cash flow, growth momentum, user engagement, and how much value you are actually creating for your customers. But unit economics (CAC & LTV) are a good way to see if your business makes sense and just how well it will scale.

Note: We are in the real world now, where data is patchy and not always reliable. This case study is based on an actual company with some details disguised. When I was preparing this series of case studies (two more coming) I talked with ten companies, but in most cases there were too many non-pricing factors at play to draw any clear conclusions. And some companies did not want to have anything made public even with identifying information removed.

Real-World Example 1: SaaS Company with Large Professional Services Component

Key Lessons

- Price increases must be coordinated with changes to the product and marketing efforts (pricing is part of an integrated strategy).

- There can be a tradeoff between different metrics. For this company, improving strategic metrics resulted in a negative effect on unit economics (you can’t always optimize everything at once — be strategic).

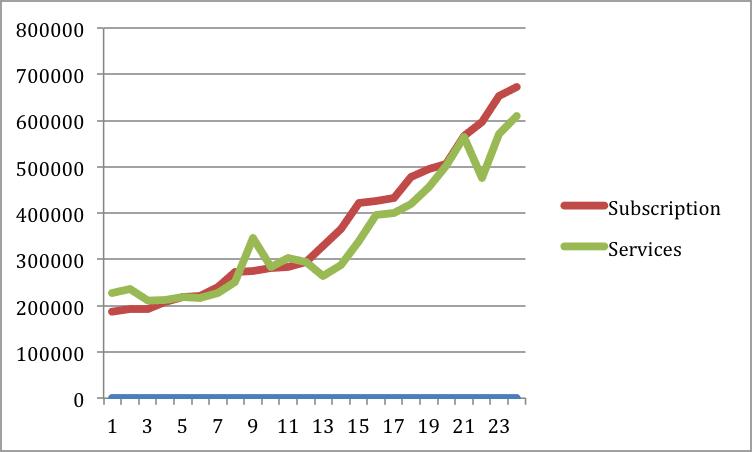

Our first case is a US B2B company that combines a SaaS platform with a relatively large professional services business. The company sells supply chain management software to makers of industrial equipment. The company has a stated strategy to increase the share of software subscriptions from about 50% of revenues to 70%. Professional services include configuration and integration and business consulting.

The price increase was made as part of a significant product upgrade and a marketing campaign that led to increased customer acquisition costs. It was part of the strategy to increase the proportion of subscription revenues. No change was made to professional services pricing, where the company tries to get 3X staff costs, but generally ends up with closer to 2.5X staff costs (yes, I know this is cost-based pricing — pricing professional services is worth a post of its own.) Anecdotally, the increase in the average value of a subscription did make it easier to sell larger professional services projects.

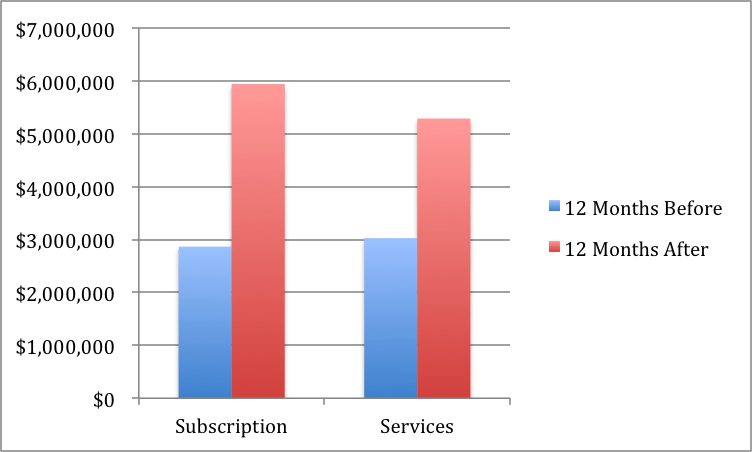

The good news: revenue growth accelerated after the price increase. But remember, the price hike coincided with a product upgrade (additional value provided to customers) and a marketing campaign dedicated to communicating the value of that upgrade. All three of those elements — the price increase, the product upgrade, and the communication — had to be planned and executed together in order to generate the observed results.

It took about two months for these changes to really impact revenues. The price increase largely held, and there was no apparent impact on discounting (this company has good sales discipline and marketing and sales work well together).

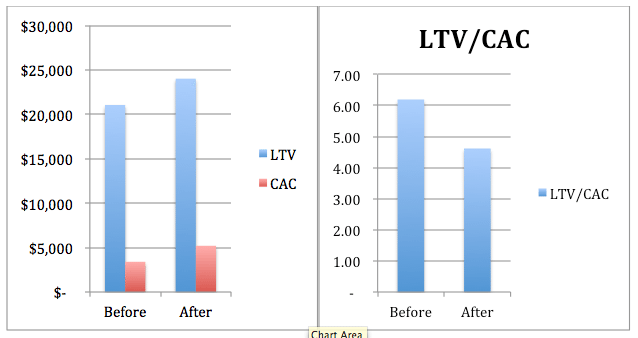

On the other hand, the unit economics were not as good after the price increase. Yes, LTV improved from $21,000 to $24,000, because of the higher selling price and an improvement in customer retention from 95% to 97%. But greater marketing efforts sent CAC from $3,400 to $5,200 and the critical LTV/CAC ratio went from a very healthy 6.2X to an adequate 4.6X.

In summary, the company implemented three coordinated actions:

- Upgraded its offer

- Increased its price

- Stepped up marketing

The results:

- Higher revenues

- More profit

- Higher customer lifetime value

- Increased customer acquisition costs

- Sharp drop in LTV/CAC ratio

Was it Worth It?

Overall, these changes helped the company to accelerate growth and shift the revenue balance from professional services to subscriptions, which is the strategic goal. The decline in unit economics was deemed acceptable, although the company does intend to keep a close eye on this and look for ways to increase LTV (it does not plan to trim marketing).

Now look at your own company and ask:

- What is the strategic metric you are working to improve and what are you willing to let slide in order to succeed with your strategic metric?

- How are your key metrics connected? If one changes (say CAC or pricing) how will this impact other metrics?

To help you estimate the impact of basic changes ahead of time, download our pricing change impact calculator.

Photo by: Maria Molinero