Why Uber is Set to Disrupt Amazon (and Other Tech Trends)

April 3, 2015

Understanding the shifts in technology and the direct impact to consumer behavior should be on the minds of any entrepreneur whether large or small.

At OpenView, we are obsessed with constantly educating ourselves on technology trends, and that led us to a presentation from Scott Galloway, Clinical Professor of Marketing at NYU Stern and L2 founder, at the DLD15 Conference. His talk is centered on the future of business and the four “horsemen” in the lead — Apple, Amazon, Facebook, and Google. We loved the talk so much that we transcribed the entire presentation for your reading pleasure.

If you want to win the race, you have to understand the players.

Transcript

At NYU Stern, we developed an algorithm in 2010 that looks at 850 data points across four dimensions, site; digital marketing; social; and mobile, and across 11 geographies. We apply this against 1,300 brands, and over the course of time, we’d like to think that we can build recommendations around who the winners and losers are, what platforms and technologies people are investing or divesting from. Sort of an always on, think of us as train spotters that see patterns in what’s going on.

In a 2% growth economy, any company that’s growing faster than 2%, there’s someone on the losing end of that. I think it’s just as important to talk about the losers as the winners. In conferences, we tend to only talk about the winners.

I affectionately call this the Four Horsemen. I was asked to look at the four most dominant companies in digital and make some sort of predictions around who’s going to increase in value and influence, and who will decrease in influence and value.

So when we say loser we just mean decrease in value or influence. Any of these companies could technically be losers for the next 10 years and still be incredibly important. They’re all amazing companies. I also want to say that I get it wrong all the time, and I constantly hear from these brands after we talk to them. I hope most of this is right, but I know some of it is wrong. Enough of the fine print…

These companies have a combined market cap of $1.3 trillion, which is greater than the GDP of South Korea, a market cap of approximately $5 million per employee. That blows away any country. If these four companies got together and created a society for their employees, it would look like something out of Elysium, the movie with Matt Damon.

Amazon

Let’s kick off and talk about Amazon.

We believe that pure play retail is going away, that ecommerce companies are either going to open stores or go out of business, and retailers need to be excellent in digital or they will go out of business.

I also believe that Amazon cannot survive as a pure play retailer.

There’s evidence everywhere. Fab raises $250 million, at a $1 billion valuation, 14 months later it’s sold for $15 million. I believe Fab, Gilt, Net-a-Porter are all fantastic companies, but once the venture capital community falls out of love with their magnetic founders and they no longer have access to cheap capital, they will discover their business models don’t work and go out of business.

Or they will open stores, and the majority of them are running to open stores. Stores are the new black, in the world of ecommerce. We’ve discovered these incredibly flexible, robust warehouses called stores. So Rent the Runway, Warby Parker and a variety of pure plays are now opening stores, the most impressive of which is Warby Parker whose sales are second in the U.S. per square foot, just behind Apple and just ahead of Tiffany.

Retailers are not befuddled prey waiting around to get disrupted. They, in fact, are growing their ecommerce businesses. This is a list of retailers that are growing their ecommerce businesses faster than Amazon. You might think Amazon’s the most innovative company in retail. Over the last 10 years that might be true, but if you look at the last five years, it’s been Macy’s from a shareholder’s standpoint. Amazon is at the lowest return of almost any major retailer in the U.S. over the last year. This is the returns of the biggest retailers in Europe, which you can take away that European retail has failed its investors.

The strategy of Amazon is the last mile strategy or last man standing. A multibillion-dollar investment, and reaching the last mile through incredible fulfillment infrastructure, hoping that other retailers have to follow them and then run out of oxygen because no other retailer has access to the same cheap capital as Amazon. However, we have revealed an Achilles heel of Amazon, Amazon’s heel, and that is their shipping costs are exploding 40% a year.

Over the last nine months Amazon’s shipping costs have gone up more than 40%, which is not sustainable even for Amazon.

Their shipping fees or what they took in for shipping was $3 billion, but they spent almost $7 billion on transportation costs. This is not sustainable. It’s a race to the bottom. They forced everybody else to offer free shipping. Two-thirds of Christmas packages were brought to you free. It used to be one-third. That happened in just 12 months.

Some of their differentiations are one-click ordering and incredible same-day fulfillment. I believe those points of differentiation are being eroded by on-demand payment and on-demand delivery.

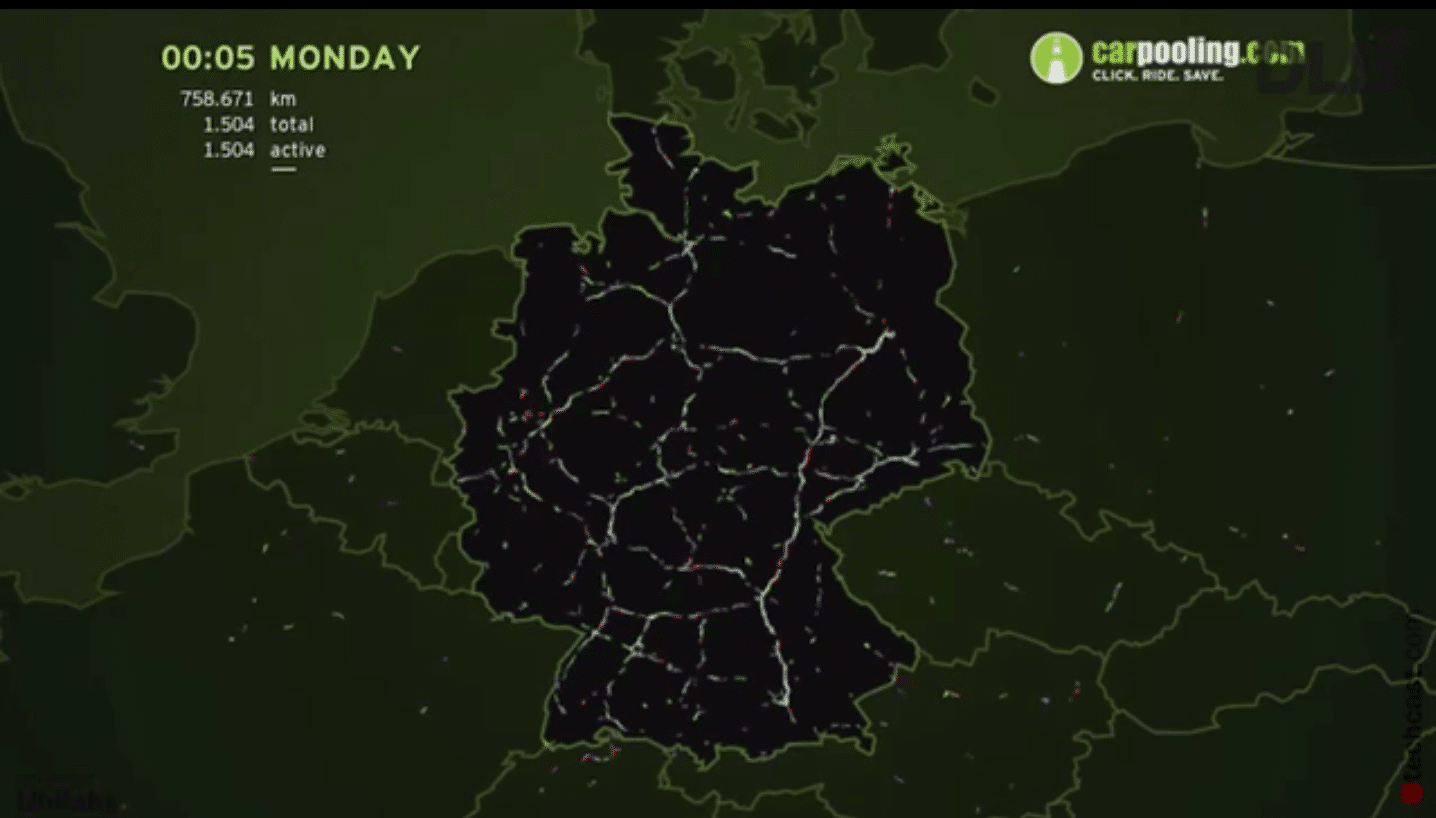

Specifically, I think, likely the disruptive force for Amazon, who’s been the most disruptive force in retail in America, is going to be Uber. It came to me, when I took an Uber ride in southern Florida and it was $4. In Chicago, you can hire a car and a driver for 90 cents a mile. If you spent the same amount on Amazon, as Amazon does on its shipping services, that’s seven billion miles of flexible delivery in the U.S.

This is a heat map of CarPoint.com, and it’s usually showing people carpooling all over Germany. What I see are not people sharing cars. I see flexible work staff, without brown or yellow DHL uniforms, who are going to be delivering packages. This guy is about to disrupt Amazon, in our view.

{kind=link}

The other big trend in retail is something pretty boring. People won’t talk about click and collect, ordering online, picking up in-store. It ends up that stores are fantastic and flexible warehouses.

Two-thirds of Europeans have tried this before. In the U.S. we’re well behind. Pickup points for online orders, drive-thru pickup points in France have exploded from 1,000 to 3,000, just in the last year. Also, stores are using their brick and mortar locations for flexible warehouses. If you order a flat screen TV from Best Buy, it will now get there faster than if you order from Amazon because they’re using their local store as the warehouse to fulfill.

The retailer of the future is not Amazon. It’s Macy’s that has multichannel retail. Macy’s is a metaphor for what’s happening not only in retail, but in our larger economy. They’re closing 15 stores, reinvesting $2 billion in online commerce. Most of these jobs are going away. They’re $40,000 to $80,000 sales jobs, and being replaced by $20,000 to $40,000 factory and fulfillment jobs.

It’s a larger metaphor for the economy where we’re losing middle class jobs. Some services jobs are going away, some growth in healthcare and education, some fantastic new jobs for people in the information economy, but where the real job growth is, is low wage, on-demand services. This [inaudible 00:06:33] economy is going to be outstanding for employment. It’s going to be terrible for wages.

Some predictions, Amazon will decline in value. Amazon will make a transformative brick and mortar acquisition, in the next 12 months because they have no choice. Pure play does not work. Top candidates are Radio Shack. My favorite is I think they will buy a gas station company and use gas stations that are decreasing in their importance, such that people can pick up their orders, or they may in fact buy or invest in the U.S. Post Office. And the music is stopping for pure play ecommerce companies.

Let’s talk about Facebook. Facebook has redefined the taxonomy of friendships.

Facebook has pulled off the greatest bait and switch in marketing history.

They convinced many of the brands in this room to spend hundreds of millions to build their communities, telling them that it would be their community and they would have access to it. They then put a walled garden around and said, “Just kidding. You have to pay for access to that community.”

The organic reach on Facebook is now 6%, meaning that if you’re Proctor & Gamble and you want to speak to the community that you paid to build, one in 16 messages will actually reach them. They are telling clients that they should assume organic reach of zero.

Best acquisitions in technology are Facebook — Instagram and WhatsApp. WhatsApp perfectly overlaps with Facebook’s weaknesses, geographically. If you want a sense for what an outstanding acquisition Instagram was, it was purchased for $100 million less than Tumblr at the same time. Facebook last year did somewhere between $400 and $500 million. Yahoo! refuses to say what Tumblr did. Best acquisition in tech, worst acquisition in tech.

The only threat to Facebook dominance — two years ago we predicted that the most powerful social network in the world would be Instagram. The primary drivers of social media are visual and being born on a mobile device, and Instagram has both.

Instagram is growing faster than any social platform with the exception of WeChat, that has over 100 million users. If you look at the Facebook properties, including Instagram that they own, they dominant the app economy.

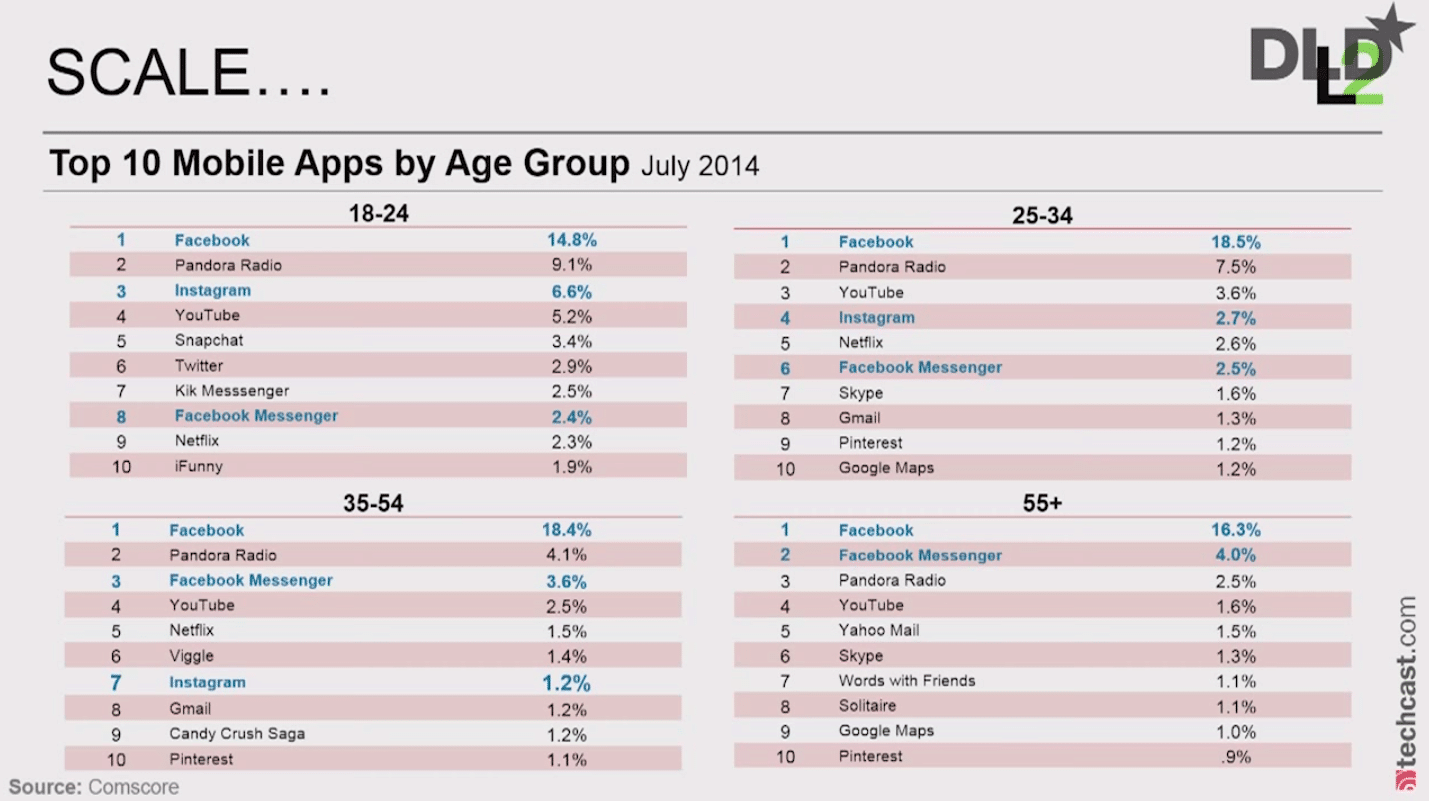

This is most popular apps by age groups. As you can see, Facebook is littered all over these charts. If you look at engagement rates, Instagram gets 10 to 15 times the engagement rate of Facebook, and 25 times the engagement rate of Twitter.

{kind=link}

Facebook loves to be picked on.

People are constantly talking about young people not liking Facebook. That is total hogwash. Facebook continues to pull away on power. Social media is becoming Facebook and the Seven Dwarves. Two-thirds of all time on social media is now on Facebook.

If you look at European nations, almost everybody that’s on a social network is on Facebook. The real quiet war that’s taking place is your ability, or Facebook and Google’s ability, to track you specifically by your identity which Google can only do on Gmail or Google+. Facebook can do it because of your specific login on Facebook, and then they can serve you ads when you’re no longer on the platform, across the wider platform. This is a huge lucrative business, and as of last year, Facebook is now tracking more individual identities than Google and beginning to pull away.

There are 1.1 billion self-identified Catholics in the world. Google has relationships with 2.2 billion people. Facebook has relationships with 2.4 billion people. The training that fits Facebook should go something like this, for the sales associates, “Hey, Big Brand, what platforms are you investing in?” “Well, we’re investing in Pinterest and Twitter.” “Congratulations, you’re going to win awards. Those are great. When you’re interested in building your brand at scale, give me a call. I have more relationships than God on this planet, and I’m on a mobile phone.”

Let’s talk about Google. Google has dominant share, but it’s beginning to decline. Other people are chipping away at their search volume — a billion searches on Facebook, 300 million searches on Twitter. Two-thirds of product searches begin on Amazon, which are high-value searches.

We see shares starting to decline.

The bottom line is the mobile economy is not friendly to Google’s business model.

When people are in apps, they’re less inclined to search on Google. As a result, the cost per click is declining. Their profits and revenues are slowing down. Google+ is dead already. It’s had a 97% decline in engagement rate.

Video — people are talking about how Facebook’s going to disrupt TV. Facebook is going to disrupt YouTube. Google Glass is not a wearable. It’s a prophylactic, ensuring you will not conceive a child, as no one will get near you.

Apple

Let’s talk about Apple. What makes the luxury brand? The first is an absolute majesty of reverence for artisanship and craft. At the very beginning there’s someone who is obsessed with a passion and a love for the craftsmanship, the art of the object itself. You also have an iconic founder. You also have an exceptionally high price point.

You have vertical control of your distribution, recognizing that brands are now built at purchase, in addition to at-broadcast media, so an exceptional investment in stores and control. Luxury for the first time last year now controls over 50% of its distribution.

You’re vertical, you’re global. Rich people are the most boring people in the world. They smell, look, and feel alike. They all fly British Airways and party in St. Bart’s. The middle class is much more different. Luxury brands are able to go global faster because rich people aspire to the same things.

I think this is the most important thing and the reason why Apple is about to become the first trillion-dollar brand. Luxury brands give you self-expressive benefit. They signal something about you. This is not a timepiece. I have not wound it in five years. It’s my vain attempt to express Italian masculinity and signal that if you mate with me I’m more likely to take care of your offspring than someone wearing a Swatch watch. We like to think we’re more evolved than that. We’re not.

The most powerful luxury brand in the world is Apple — craftsmanship, an iconic founder, exceptional price point. Find another technology product that over time, as it’s matured, has expanded its margins. This is the only tech product I can find that’s been able to achieve that.

Exceptional price point, control of their distribution, and they opened stores just 13 years ago, now the most successful retailer in the store. The store I’m looking at here on Fifth Avenue will do half a billion dollars just in this one underground store. It’s very much a global brand, with exceptional brand management, and core associations that extend beyond cultural boundaries.

What’s the key? The self-expressive benefit. It’s no accident they hired Paul Deneve out of YSL, or Angela Ahrendts was willing to give up a $28 million dollar job and move to Cupertino. She’s not opening stores. She’s building the next great luxury brand. Look how Burberry-esque this Apple watch ad looks.

{kind=link}

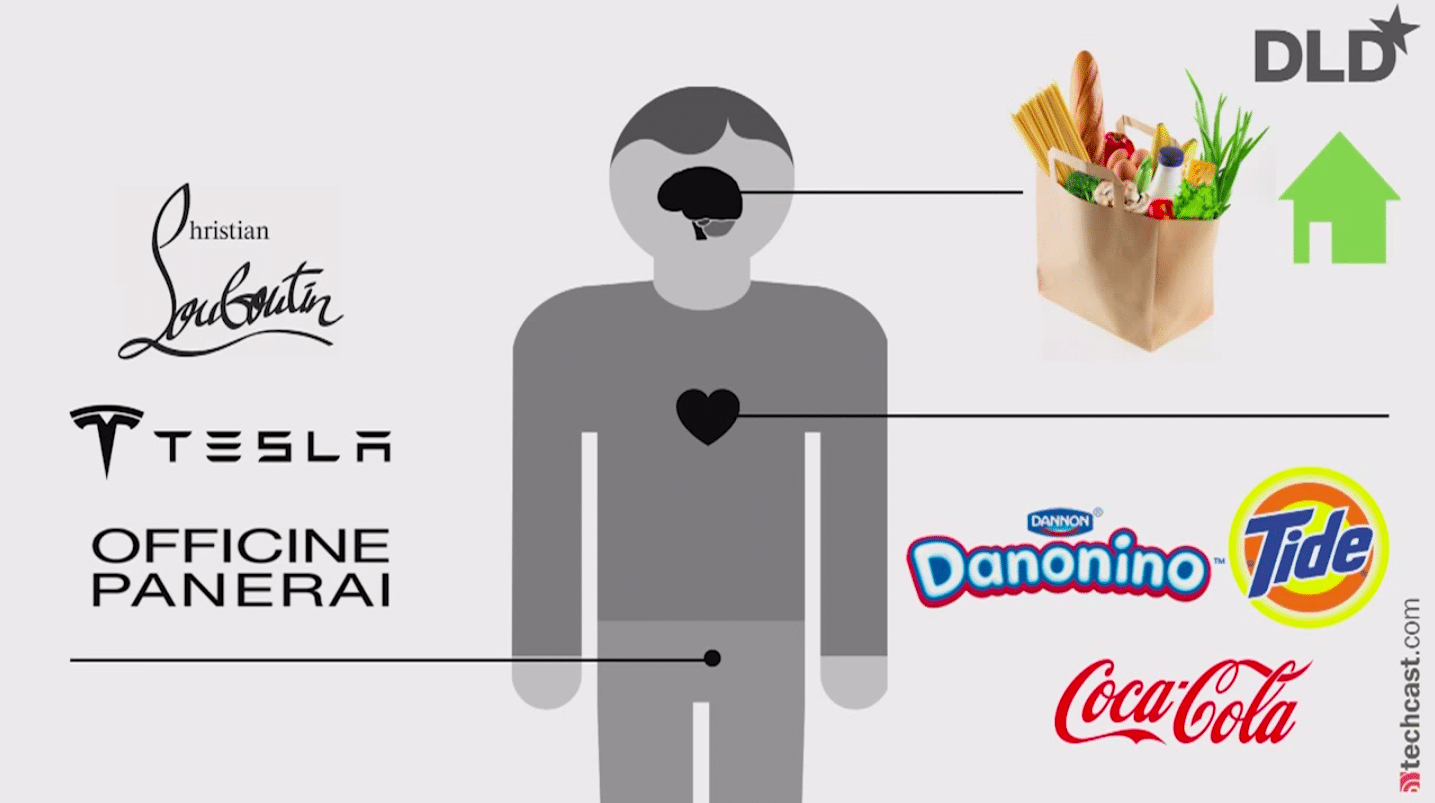

Self-expressive benefit. There are only three things we do in business, and that’s appeal to:

- People’s instinct to survive: food, housing, warmth, clothing, etc.

- Their ability and instinct to love: Choosy moms choose Jif. Buy Tide. If the clothes are washed with Tide, it shows that you love your family.

- And your desire to propagate.

As you move down the torso, the margins get better, and the business gets better…. Apple is the only tech company in history that has successfully migrated down that torso.

Tesla is not an environmental car. It’s an attempt to tell people you can afford a $120,000 car. The core axiom of evolution is men paying $150,000 for cars that can go 160 miles an hour in domains where you can only go 55. It makes no sense. Women will continue to pay $600 for ergonomically impossible shoes to try to solicit inbound offers from those same men. Don’t laugh. I believe this stuff.

Apple is the only tech company in history that has successfully migrated down that torso. It used to be the best computer. Then it sang to your heart with songs. Now it’s the ultimate self-expressive benefit brand.

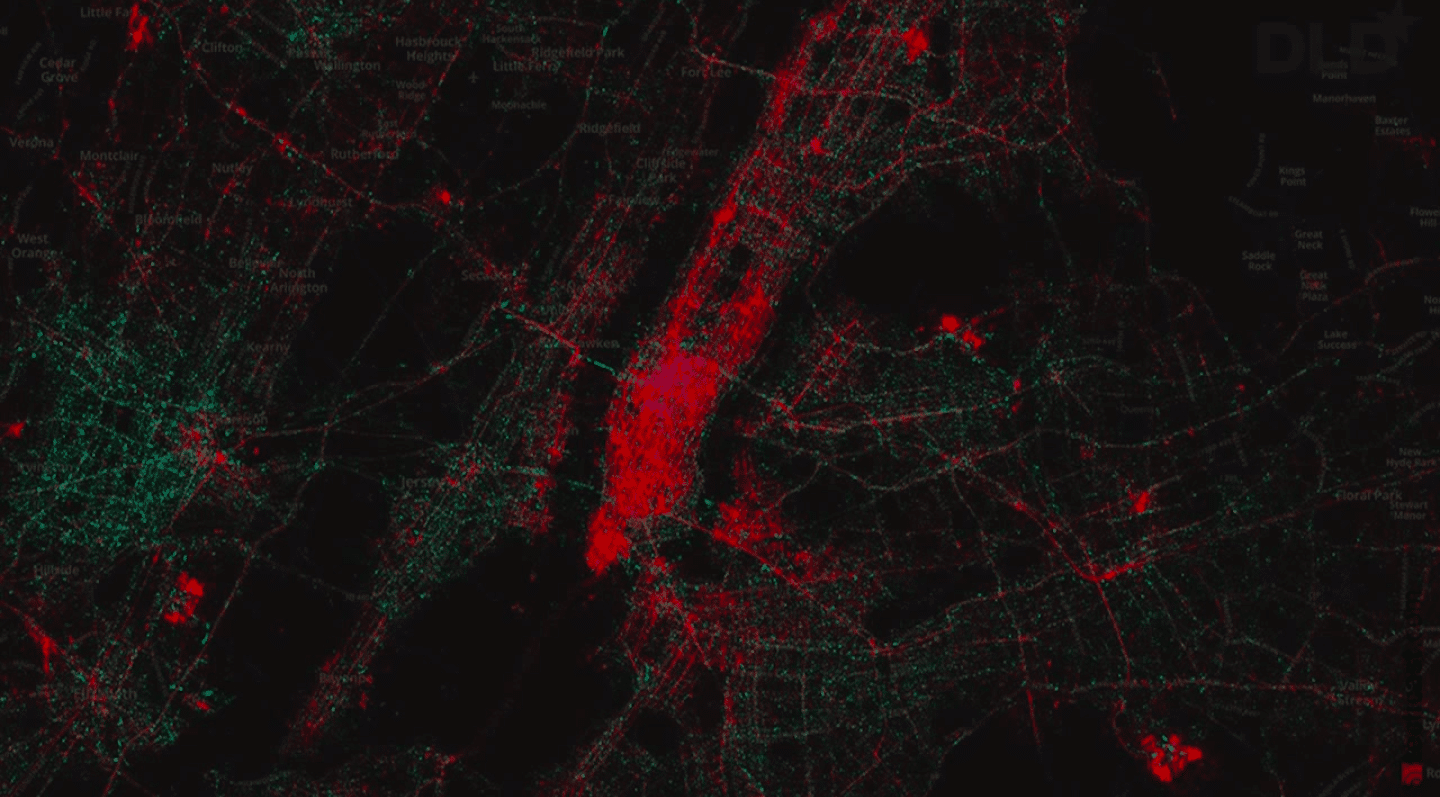

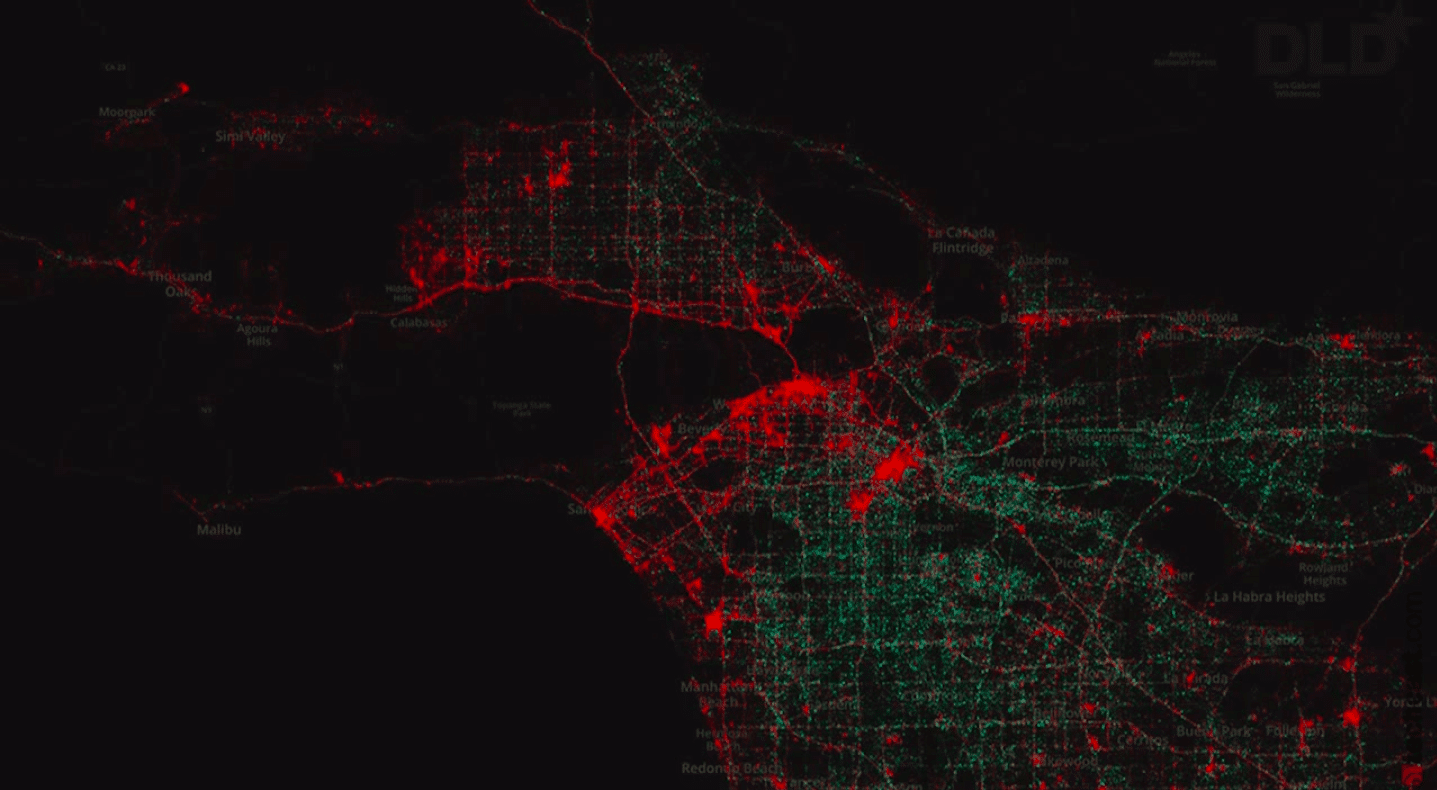

This is a heat map of operating systems. This is the iOS operating system. The wealthy areas in Manhattan, and as you go into the lower income households in suburbia, Android lights up. By the way, if you see purple in the middle, that’s Jurassic Park. That’s the dinosaurs using Blackberry.

{kind=link}

This is Los Angeles. If you want to live on the coast or in Beverly Hills you have to own an iOS. If you want to move inland or into South Central, you can use Android.

{kind=link}

The ultimate self-expressive benefit brand is now an iPhone. For those of you carrying an iPhone, it means you’re wealthier and better educated, and more likely to have more options in terms of who you mate with. We knew they were going into watches. Do you want to see a company in denial? Talk to the watch industry.

I’m going to fly through this. The first year, Apple’s going to be the biggest watch company in the world. Who does this hurt? It hurts everybody. Not just watch companies, but all aspirational price point brands. Teen retailers have been getting killed. They’re staring at their navel. Is it a product? Is it a brand problem? It’s an Apple problem. These brands get hurt.

Predictions — Apple will become the first trillion-dollar market cap company on the back of its successful transition to a luxury brand. The luxury broom hits a wall, China, lack of innovation, Apple.

My name is Scott Galloway. I teach in NYU Stern. I appreciate your time.